Today, ATMs have become a key element of the payment infrastructure and play a vital role in the development of electronic payments and the digital transformation of the entire financial sector. Furthermore, expanding the ATM network ensures basic access to financial services in the regions, including for socially vulnerable groups, thereby reducing digital inequality.

Based on the above trends, the commercial banks, together with the UZCARD payment system, are consistently expanding the ATM network throughout the country.

For many users, their acquaintance with plastic cards begins with using ATMs which fosters the habit of making electronic transactions. ATMs provide 24/7 access to users’ funds and create a ‘soft transition’, building trust in cards and, ultimately, in electronic payments. At the same time, despite the development of mobile and online payment channels, ATMs are evolving from simple cash dispensers into multifunctional self-service centers integrated into the modern digital banking ecosystem.

Thus, currently, using ATMs you can not only withdraw cash, but also check your card balance, receive account statements, pay public utility bills, deposit cash into card accounts, exchange currencies, and much more.

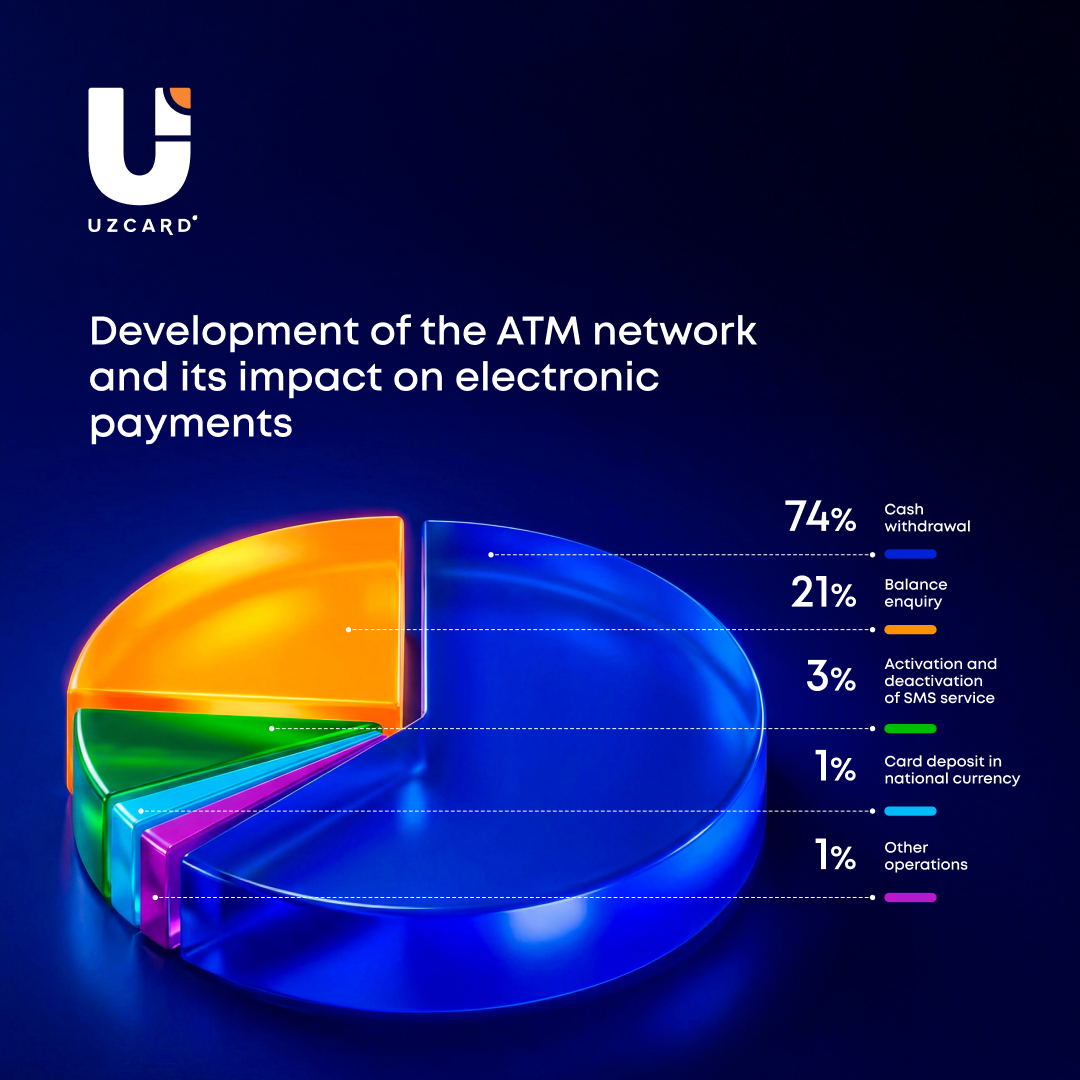

The analysis of transactions processed through UZCARD ATMs shows that cash withdrawals account for 74% of total ATM transactions. This indicates consistently high demand for basic cash transactions and confirms the importance of the ATM network for the population. Last year, over 120 trillion UZS in cash were dispensed through ATMs, a 21% increase compared to the year before.

At the same time, the transaction structure demonstrates a gradual shift from a narrow function to a multifunctional self-service model. Specifically, in addition to cash withdrawals, a significant portion of transactions are made up of balance inquiries, as well as activation and deactivation of SMS service, card top-ups by depositing the national currency, and more.

Over 51 million card balance inquiries were processed through ATMs, making this operation’s share of all transactions 21%. Moreover, a significant increase in transactions compared to 2024 figures was observed for the “SMS Service Activation and Deactivation” service – 29.8%, with the total number of transactions exceeding 8 million. This trend demonstrates the growing popularity of electronic payments among cardholders, as the service is used at ATMs to enable card balance monitoring and the ability to link cards to a mobile app.

Regarding the user structure by issuers, it is worth noting that in 2025, the “SMS Service Activation” service was most widely used by Xalq Bank cardholders, with the share of 28%. Agro Bank users followed with 21%, and NBU and OTP Ipoteka Bank cardholders each accounted for 10%.

Thus, based on the transaction analysis, it can be concluded that the ATM network is becoming an important factor in integrating electronic payments into everyday life and is positively influencing the financial and digital literacy of the population.